Introduction to PITI in Real Estate

If you are buying a property or refinancing a current mortgage, you might have come across a term called PITI.

This is a very general but one of the most significant terms in the mortgage industry as it is used as one of the qualification parameters by lenders. In this post, we will understand what is PITI in a mortgage in detail.

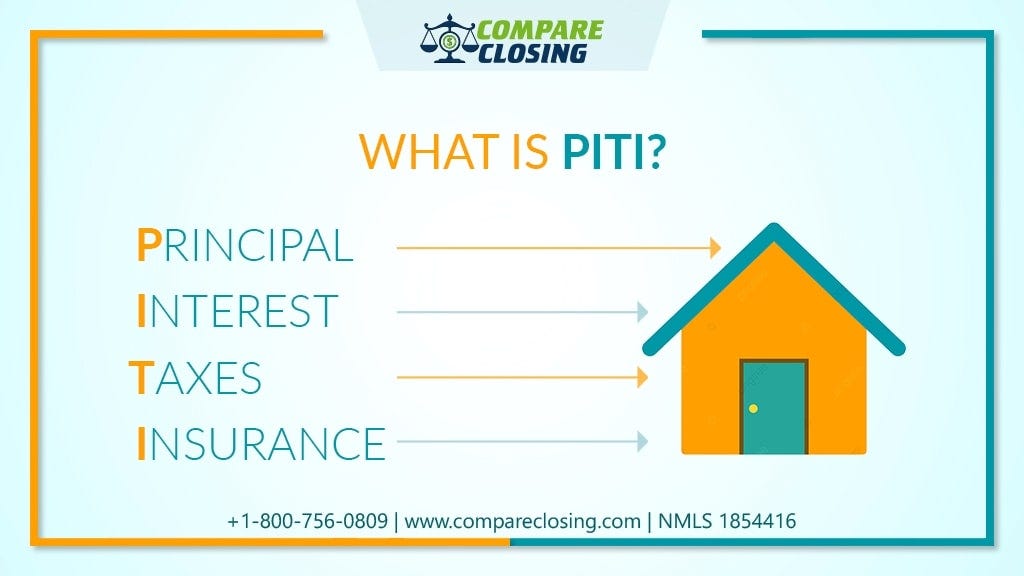

What Is PITI? And What Does PITI Stand For?

When you take out a mortgage your monthly payments usually include principal, interest, taxes, and insurance.

PITI is an abbreviation for the same. Most of the lenders will have your PITI as a qualifying parameter for the front-end DTI.

Now since we know what PITI stands for, let us understand what each one of these items means.

Principal (P):

Principal is the total number of money that is borrowed from the lender by the borrower.

For example, if you have borrowed $250,000 to purchase a property, your principal amount is going to be $250,000.

When you make your monthly mortgage payment, a portion of the payment goes towards paying down your principal amount.

The principal amount portion in your monthly payment remains the same for the tenure of the mortgage.

Interest (I):

I stand for interest. Interest is the amount charged by the lender to borrow the money to buy the property.

The interest rate charged to the borrower depends on multiple factors, like credit scores, the loan amount and loan to value ratio, and your debt to income ratio.

When you are taking out a mortgage, there are two types of interest rates the borrower can opt for, an adjustable-rate mortgage and a fixed-rate mortgage.

In the fixed-rate mortgage, the interest rate remains unchanged for the entire tenure of the loan.

In the adjustable-rate mortgage, the interest rate is fixed for the initial period of the loan, and then it adjusts as per the market after the fixed period is over.

This means that if the market rate is higher your payments could go up. However, if the market index is low, your monthly payment could go lower.

Property Taxes (T):

T stands for property taxes. Your property tax is something that you have to pay on your property to your county.

Depending on the state you live in your property taxes are due to be paid every six months or once a year. It is up to the borrower to decide whether he/she wants to include the property taxes in the monthly mortgage payment or pay them directly to the county.

If you decide to include that in your monthly mortgage payment, your lender will set up a separate account known as an escrow account where these taxes would be collected monthly and will be paid by the lender to the county once they are due.

Your county appraisal district will determine the tax rate in your area and your property. If the tax rate increases your monthly payment will increase as well. If the tax rate decreases, your monthly mortgage payment will decrease as well.

Insurance (I):

When it comes to the protection of your home and prized possessions within the home, it is suggested to have homeowner’s insurance for your property.

The insurance helps to protect your home from fire, break-ins, storms, floods, and earthquakes.

Some insurance also helps to cover your priced possessions like jewelry, exclusive artwork, etc. by paying additional coverage also known as a rider.

In case you live in a condominium, your dwelling cover is included in the homeowner association fees. Just like property taxes, your insurance amount is collected by the lender every month through an escrow account, and will pay it to the insurance company when it is due.

The calculation of the insurance amount depends on a lot of factors, like property value, location of the property, available amenities in the area, etc.

Another type of insurance could be included in your monthly mortgage payments is mortgage insurance.

This insurance payment becomes part of your monthly mortgage payment if you have made less than a twenty percent down payment while purchasing the property.

Conclusion

Home buying is one of the biggest decisions you make in your life and principal, interest, taxes, and insurance plays a very significant role in the home buying process.

Understanding what your principal, interest, taxes, and insurance are going to be will help you to determine if the home that you are planning to buy is affordable.

Speak to your trusted loan officer who would be in a position to help you know what is your principal, interest, taxes, and insurance, and if you can qualify for the home that you are planning to buy.

https://www.compareclosing.com/blog/what-is-piti-in-real-estate/

Comments

Post a Comment